Understanding Home Equity Loans in the United States

A home equity loan is a type of loan that allows homeowners to borrow against the equity they have built up in their property. Equity is the difference between the home's current market value and the outstanding balance of any mortgages or liens on the property. Home equity loans are popular in the United States because they often come with lower interest rates compared to other types of loans, making them an attractive option for financing major expenses such as home improvements, debt consolidation, or education costs. This article provides a comprehensive guide to understanding home equity loans, their benefits, risks, and the application process in the United States.

What Is a Home Equity Loan?

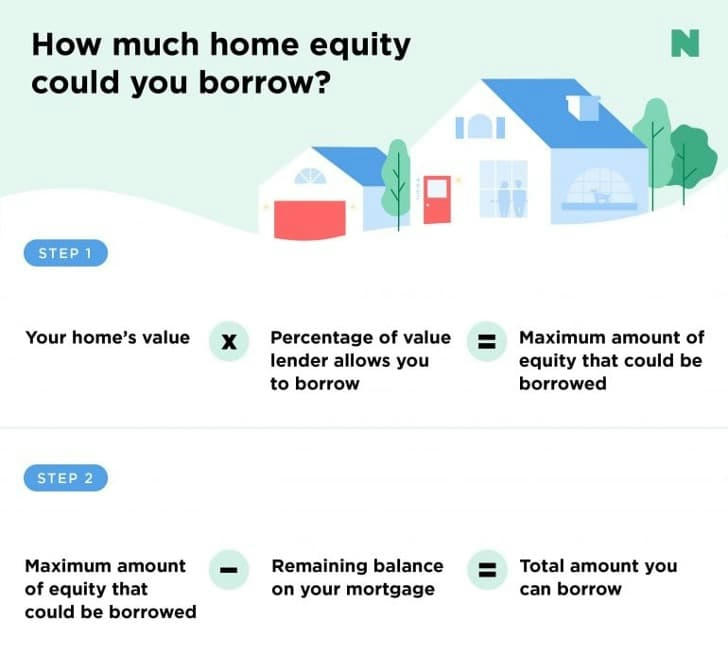

A home equity loan, also known as a second mortgage, allows homeowners to borrow a lump sum of money using their home as collateral. The loan amount is determined by the amount of equity the homeowner has in the property. For example, if a home is valued at 300,000 and the home owner owes 200,000 on their mortgage, they have $100,000 in equity. Lenders typically allow borrowers to access up to 85% of this equity, depending on their creditworthiness and other factors.

Home equity loans are different from home equity lines of credit (HELOCs). While a home equity loan provides a lump sum with a fixed interest rate and fixed monthly payments, a HELOC operates more like a credit card, allowing borrowers to draw funds as needed up to a certain limit and repay them over time.

Benefits of Home Equity Loans

Lower Interest Rates: Home equity loans generally offer lower interest rates compared to personal loans, credit cards, or other unsecured loans because the loan is secured by the property. This makes them a cost-effective option for borrowing large sums of money.

Fixed Interest Rates and Payments: Unlike HELOCs, which often have variable interest rates, home equity loans typically come with fixed interest rates and fixed monthly payments. This predictability makes it easier for borrowers to budget and plan their finances.

Tax Deductibility: In some cases, the interest paid on a home equity loan may be tax-deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. However, tax laws can change, so it's important to consult a tax advisor for the most up-to-date information.

Flexible Use of Funds: Home equity loans can be used for a variety of purposes, including home renovations, debt consolidation, medical expenses, education costs, or even major life events like weddings. This flexibility makes them a versatile financial tool.

Potential to Increase Home Value: If the loan is used for home improvements, it can increase the property's market value, potentially boosting the homeowner's equity even further.

Risks of Home Equity Loans

Risk of Foreclosure: Since the home serves as collateral, failure to repay the loan could result in foreclosure. This makes it crucial for borrowers to ensure they can afford the monthly payments before taking out a home equity loan.

Closing Costs and Fees: Similar to a primary mortgage, home equity loans often come with closing costs, which can include appraisal fees, origination fees, and other administrative expenses. These costs can add up, so borrowers should factor them into their decision.

Reduced Equity: Borrowing against home equity reduces the amount of equity the homeowner has in their property. This can be a disadvantage if the homeowner plans to sell the home in the near future or needs to access additional funds later.

Potential for Overborrowing: The availability of a large lump sum can tempt some borrowers to take on more debt than they can comfortably repay, leading to financial strain.

Eligibility Requirements for Home Equity Loans

To qualify for a home equity loan in the United States, borrowers typically need to meet the following criteria:

Good Credit Score: A credit score of 620 or higher is generally required, though some lenders may prefer scores of 700 or above for the best interest rates.

Stable Income: Borrowers must demonstrate a stable income and the ability to repay the loan. Lenders will typically review pay stubs, tax returns, and other financial documents.

Low Debt-to-Income Ratio: Lenders prefer borrowers with a low debt-to-income (DTI) ratio, typically below 43%. This ratio measures the borrower's monthly debt payments relative to their income.

Property Appraisal: The lender will usually require an appraisal to determine the home's current market value and ensure it meets their lending criteria.

How to Apply for a Home Equity Loan

The process of applying for a home equity loan in the United States involves several steps:

Check Credit Score: Before applying, borrowers should review their credit report and score to ensure they meet the lender's requirements. Any errors on the credit report should be disputed and corrected.

Calculate Equity: Borrowers should determine how much equity they have in their home by subtracting the outstanding mortgage balance from the home's current market value.

Shop Around: It's important to compare offers from multiple lenders, including banks, credit unions, and online lenders. Borrowers should compare interest rates, fees, loan terms, and customer reviews.

Gather Documentation: Lenders will require documentation such as proof of income, tax returns, bank statements, and identification. Borrowers should have these documents ready to expedite the application process.

Submit Application: Once a lender is chosen, borrowers can submit their application, either online or in person. The lender will review the application and may request additional information.

Home Appraisal: The lender will arrange for a professional appraisal of the property to determine its current market value.

Loan Approval and Closing: If approved, the borrower will receive a loan agreement outlining the terms and conditions. After signing the agreement and paying any closing costs, the loan funds will be disbursed as a lump sum.

Alternatives to Home Equity Loans

While home equity loans are a popular option, they may not be suitable for everyone. Some alternatives include:

Home Equity Line of Credit (HELOC): A HELOC provides a revolving line of credit that can be drawn upon as needed, making it a flexible option for ongoing expenses.

Cash-Out Refinance: This involves refinancing the existing mortgage for a higher amount than the current balance and receiving the difference in cash. It can be a good option if mortgage rates are lower than home equity loan rates.

Personal Loans: Unsecured personal loans do not require collateral but typically come with higher interest rates and shorter repayment terms.

Credit Cards: For smaller expenses, credit cards may be a convenient option, though they often have higher interest rates compared to home equity loans.

Conclusion:

Home equity loans are a powerful financial tool for homeowners in the United States, offering access to funds at relatively low interest rates. They can be used for a wide range of purposes, from home improvements to debt consolidation, and provide the benefit of fixed monthly payments. However, they also come with risks, such as the potential for foreclosure and reduced home equity.

Before applying for a home equity loan, borrowers should carefully evaluate their financial situation, compare offers from multiple lenders, and consider alternatives if necessary. By understanding the benefits, risks, and application process, homeowners can make informed decisions and use home equity loans to achieve their financial goals responsibly.