💰 Everything You Need to Know About Debt Consolidation Loans

Debt can accumulate quickly, and managing multiple monthly payments with different interest rates can be overwhelming. This is where debt consolidation loans can make a difference. This type of loan allows you to combine multiple debts into a single monthly payment, often with a lower interest rate, making it easier to manage your personal finances.

According to a report by Experian, the average American carries a credit card balance of around $6,500, with interest rates often exceeding 20%. If you are struggling with multiple debts, a consolidation loan might help you save money and regain control of your finances.

📌 What is a Debt Consolidation Loan?

A debt consolidation loan is a type of financing that allows you to pay off multiple debts simultaneously. Instead of making separate payments to different creditors, you get a single loan with a fixed or variable interest rate. This can simplify debt management and, in many cases, reduce the total amount of interest you pay over time.

🔹 Example: If you have three credit cards with interest rates of 20%, 22%, and 25%, you could consolidate them into a loan with a 12% rate, significantly reducing the interest you pay monthly. Over a year, this could save you hundreds or even thousands of dollars in interest payments.

📊 Benefits of Debt Consolidation

✔ Simplified Payments: One single monthly payment instead of multiple ones.

✔ Lower Interest Rate: Less interest paid over time.

✔ Reduced Financial Stress: Makes budgeting easier.

✔ Potential Credit Score Improvement: Paying off debts faster and reducing credit utilization can help boost your score.

✔ Fixed Repayment Schedule: Unlike credit cards with revolving balances, a consolidation loan comes with a clear payoff date, helping you stay on track.

💡 Did You Know? The Federal Reserve reports that the average personal loan interest rate is around 10.7%, much lower than most credit card rates, making debt consolidation a great option for those with high-interest credit card debt.

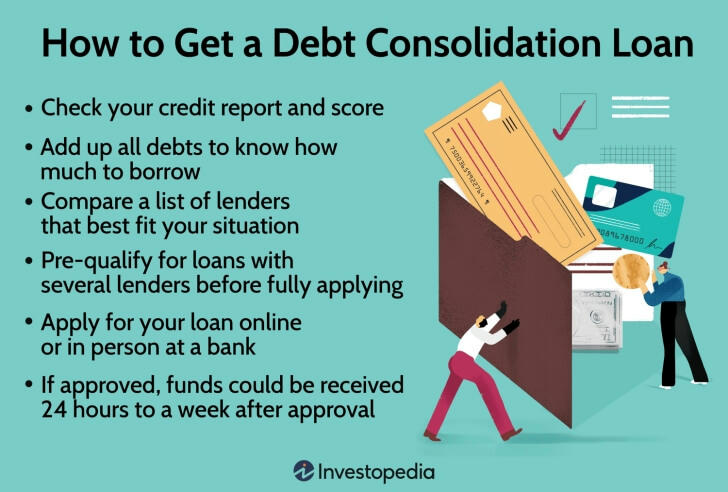

💳 How Does a Debt Consolidation Loan Work?

1️⃣ Evaluate Your Financial Situation: List all your debts and interest rates.

2️⃣ Compare Loan Options: Look for banks, credit unions, and online lenders.

3️⃣ Apply for the Loan: Submit financial documents such as income proof and account statements.

4️⃣ Pay Off Your Existing Debts: Use the loan funds to settle outstanding balances.

5️⃣ Make Timely Payments: Stay on top of your new loan payments to avoid extra fees.

🏦 Types of Debt Consolidation Loans

📌 Personal Loans: A common option available through banks and online lenders. Loan amounts typically range from $2,000 to $50,000, with repayment terms from 12 to 60 months.

📌 Home Equity Lines of Credit (HELOCs): Use your home's value to secure a lower interest rate, often between 3% and 8%, but your home serves as collateral.

📌 Balance Transfer Credit Cards: Some cards offer 0% interest for 12-18 months, allowing you to pay off high-interest credit card debt without accruing more interest.

📌 Debt Consolidation Programs: Some specialized companies negotiate lower interest rates with creditors, though they may charge fees for their services.

💡 Pro Tip: If you opt for a balance transfer card, ensure you pay off the balance before the promotional period ends to avoid high interest rates afterward.

📉 Is Debt Consolidation Right for You?

💡 It’s a good option if:

✅ You’re paying high-interest rates.

✅ Managing multiple payments is difficult.

✅ You want to reduce interest payments over time.

✅ You have a stable income and can commit to a repayment plan.

⚠ It may not be ideal if:

❌ Your spending habits are not under control.

❌ You don’t qualify for a lower interest rate.

❌ You’re on the verge of bankruptcy and need other financial assistance.

❌ You are unable to make consistent payments, which could lead to further financial struggles.

According to a Bankrate survey, 60% of Americans with credit card debt are looking for ways to consolidate their loans, making it a popular choice for those seeking financial stability.

📢 Conclusion

Consolidating your debts can be an effective strategy to lower monthly payments and simplify your finances. However, it’s important to research available options and choose the one that best fits your situation. If you’re struggling with multiple debts and high interest rates, a debt consolidation loan might be the solution you need to regain control of your finances.

📌 Final Tip: Before making a decision, compare offers from different lenders and carefully read the terms and conditions. Start your journey toward a healthier financial life today! 💪💲